- +91 8169745890

-

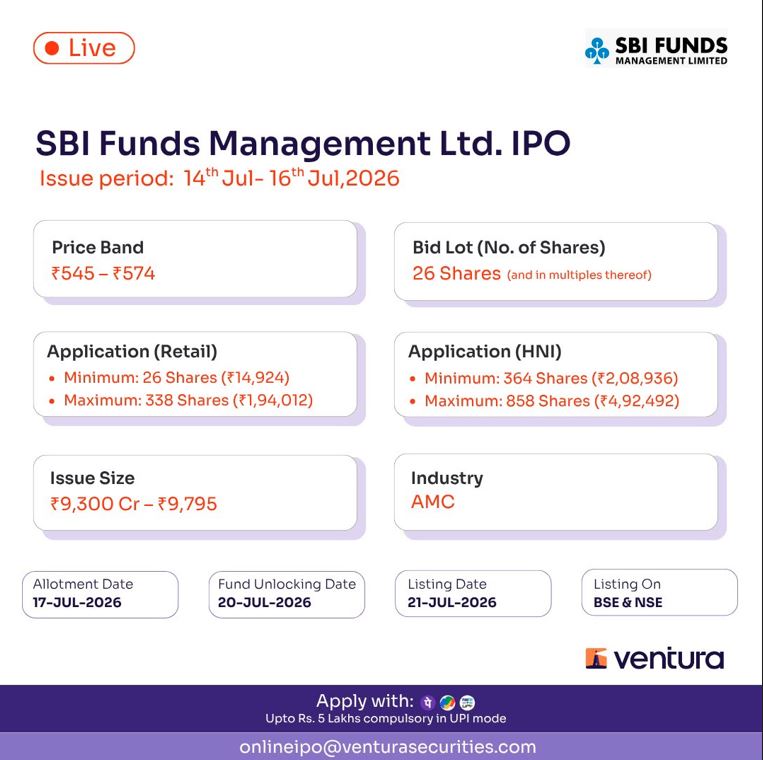

.png)

Financial Protection: Should the insured pass away within the policy's term, term insurance pays a lump sum payment (also known as a death benefit) to the nominee. This sum can assist in making up for the lost income and giving the family financial stability so they can continue to meet their responsibilities and retain their way of life. The best part is that term insurance plans cost less than a lot of other life insurance products. You pay as little as 2 percent of your annual income for such a coverage, that’s 20 times more than your current annual income.

Affordability: When compared to other life insurance policy types, term insurance usually gives a high coverage level at a comparatively low cost. Because of its cost, a broad spectrum of people, especially young people, and those on a tight budget, may buy it. Term insurance premiums are deductible from income up to a specific amount under Section 80C of the Income Tax Act. It is also an effective tax-saving tool because the nominee's death benefit is often tax-free under Section 10(10D).

Financial Replacement: When a family's principal provider passes away, their dependents may suffer greatly from a lack of money. By helping to restore this lost income, term insurance helps make sure that the family's basic needs—such as a mortgage, schooling costs, and everyday expenses—are met. You may utilize term insurance to pay off existing debts, including personal, auto, and house loans. The family can utilize the death benefit in the case of the insured's passing to pay off these obligations, relieving them of some of the financial load.

Flexible Options: Depending on a policyholder's needs and financial objectives, term insurance policies frequently offer flexible options for determining the coverage level, policy duration, and frequency of premium payments. According to needs, riders or extra benefits can also be added to the coverage to improve it. A lump sum payment is made upon the diagnosis of any qualifying critical illness under some term insurance policies' critical illness coverage. If the policyholder lives out the policy term, certain term insurance policies include a return of premium option, in which case the premiums paid are reimbursed.

Remember that it's critical to select a term insurance plan that best suits your requirements both personally and financially. Before making a choice, make sure you have properly read the terms and conditions of the policy.

Tags : ,

Started our journey back in 2008 with a goal of helping people grow their wealth as well as protect it. Catering to 400+ clients locally and internationally, Fine Investments is a one stop shop for all your financial investment needs.

Office No. 705, A-wing, AUM Avenue, MG Road, Near Ambaji Dham Mandir, Mulund West, Mumbai 400080

+91 8169745890

+91 8454941139

Copyright © Fine Investments. All rights reserved.

Risk Factors – Investments in Mutual Funds are subject to Market Risks. Read all scheme related documents carefully before investing. Mutual Fund Schemes do not assure or guarantee any returns. Past performances of any Mutual Fund Scheme may or may not be sustained in future. There is no guarantee that the investment objective of any suggested scheme shall be achieved. All existing and prospective investors are advised to check and evaluate the Exit loads and other cost structure (TER) applicable at the time of making the investment before finalizing on any investment decision for Mutual Funds schemes. We deal in Regular Plans only for Mutual Fund Schemes and earn a Trailing Commission on client investments. Disclosure For Commission earnings is made to clients at the time of investments.

AMFI Registered Mutual Fund Distributor – ARN-60554 | Date of initial registration ARN – 03-Dec-2010 | Current validity of ARN – 09-Apr-2028

Grievance Officer- Hitesh Shah | hitesh.fineinvestments@gmail.com

Important Links | Disclaimer | Disclosure | Privacy Policy | SID/SAI/KIM | Code of Conduct | SEBI Circulars | AMFI Risk Factors